.svg)

.svg)

What is the ultimate definition of primacy? If your answer is “capturing a customer’s direct deposit,” you’re not alone. In a recent webinar, 83% of attendees agreed. However, Pinwheel data shows that it’s time to evolve our definition of primacy.

Direct deposits and primary bills: a symbiotic relationship

While direct deposits have long been considered a cornerstone of account primacy, Pinwheel’s experience in completing millions of switches uncovered a surprising finding: many customers who complete a direct deposit do not end up demonstrating other high-engagement behaviors typically associated with a primary account. While in theory the direct deposit indicates the account is primary, in practice the account is secondary.

This insight led us to uncover another critical finding: to achieve true account primacy, in addition to securing a customer’s direct deposit, financial institutions must also prioritize capturing their customer’s’ recurring payments such as rent, mortgages, utilities, internet, and subscriptions. These primary bills represent the majority of a customer’s monthly spending and serve as strong indicators of the customer’s financial engagement with their bank. In fact, a recent Javelin study asked consumers how they determine their primary bank account, and the #1 response was “where I pay most of my bills.”

Timing is everything

Direct deposits and primary bills are not competing priorities—banks need them both to achieve primacy, and capturing them early on in the customer lifecycle is key. Pinwheel data shows that if a customer's direct deposit and at least some number of their primary bills are not secured within the first 60 days, retention drops by ~50%. To achieve meaningful account primacy and reduce attrition, financial institutions need to capture customer deposits and bills as close to the time of account opening as possible.

Introducing the Pinwheel Switch Kit

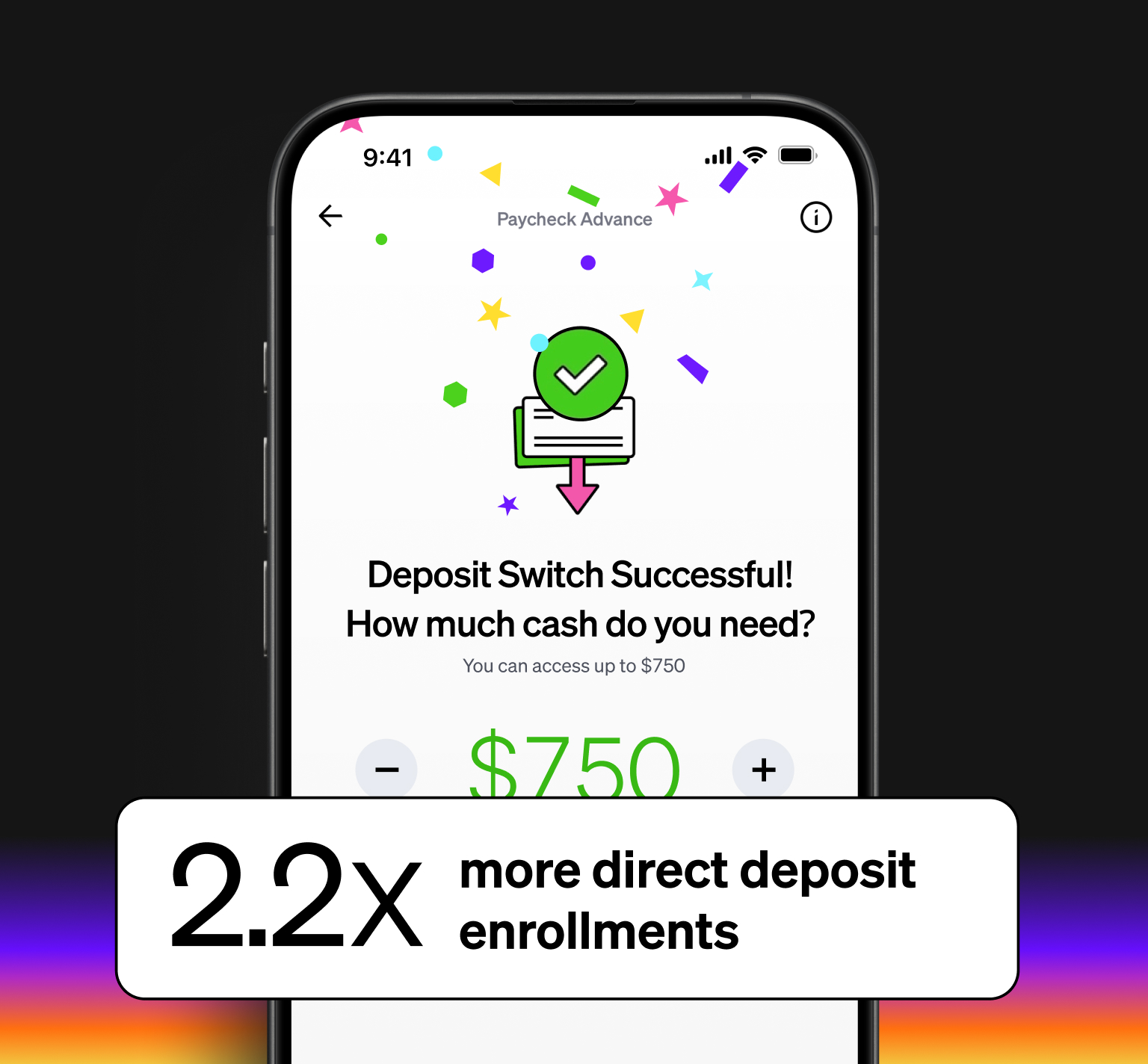

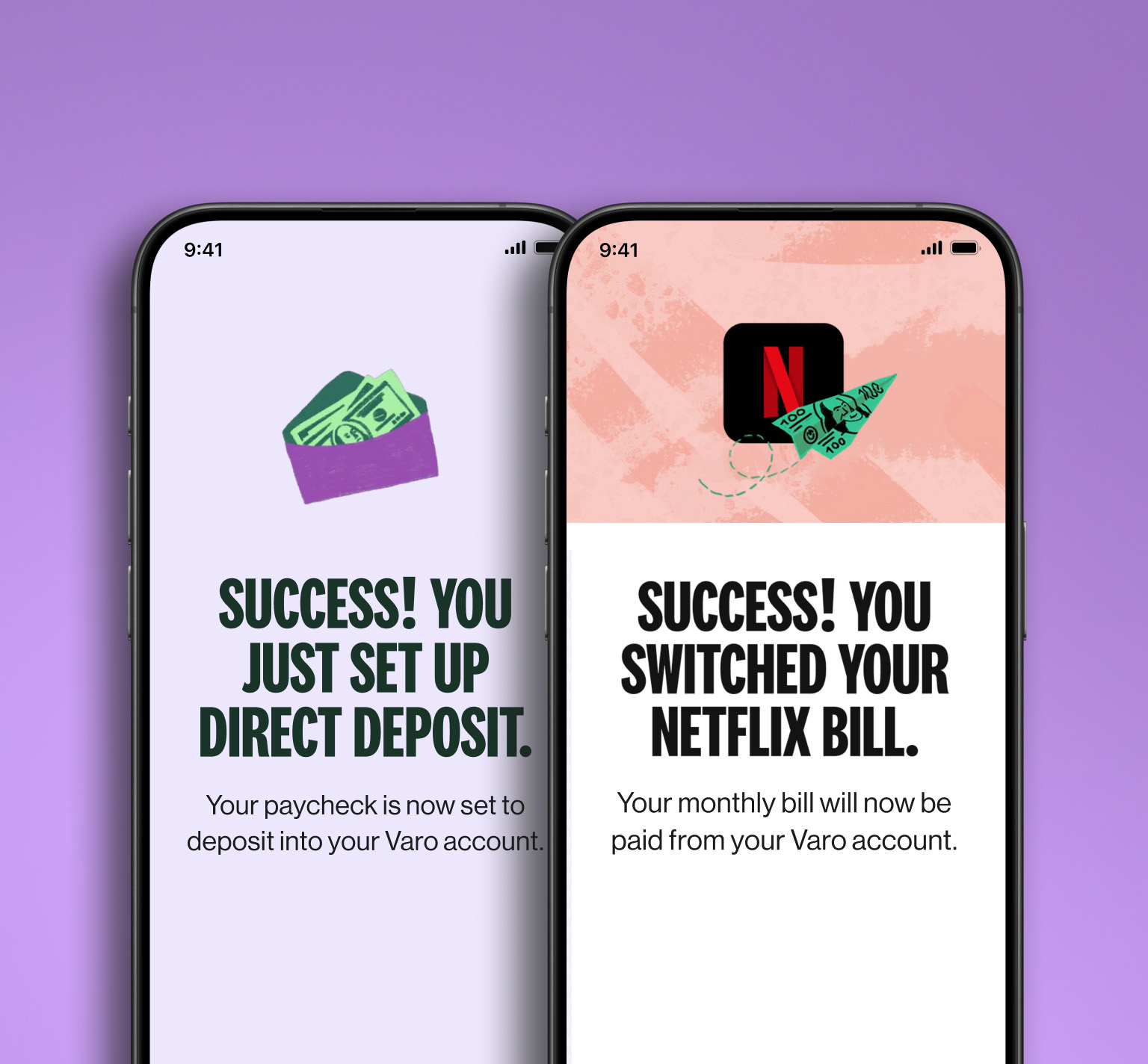

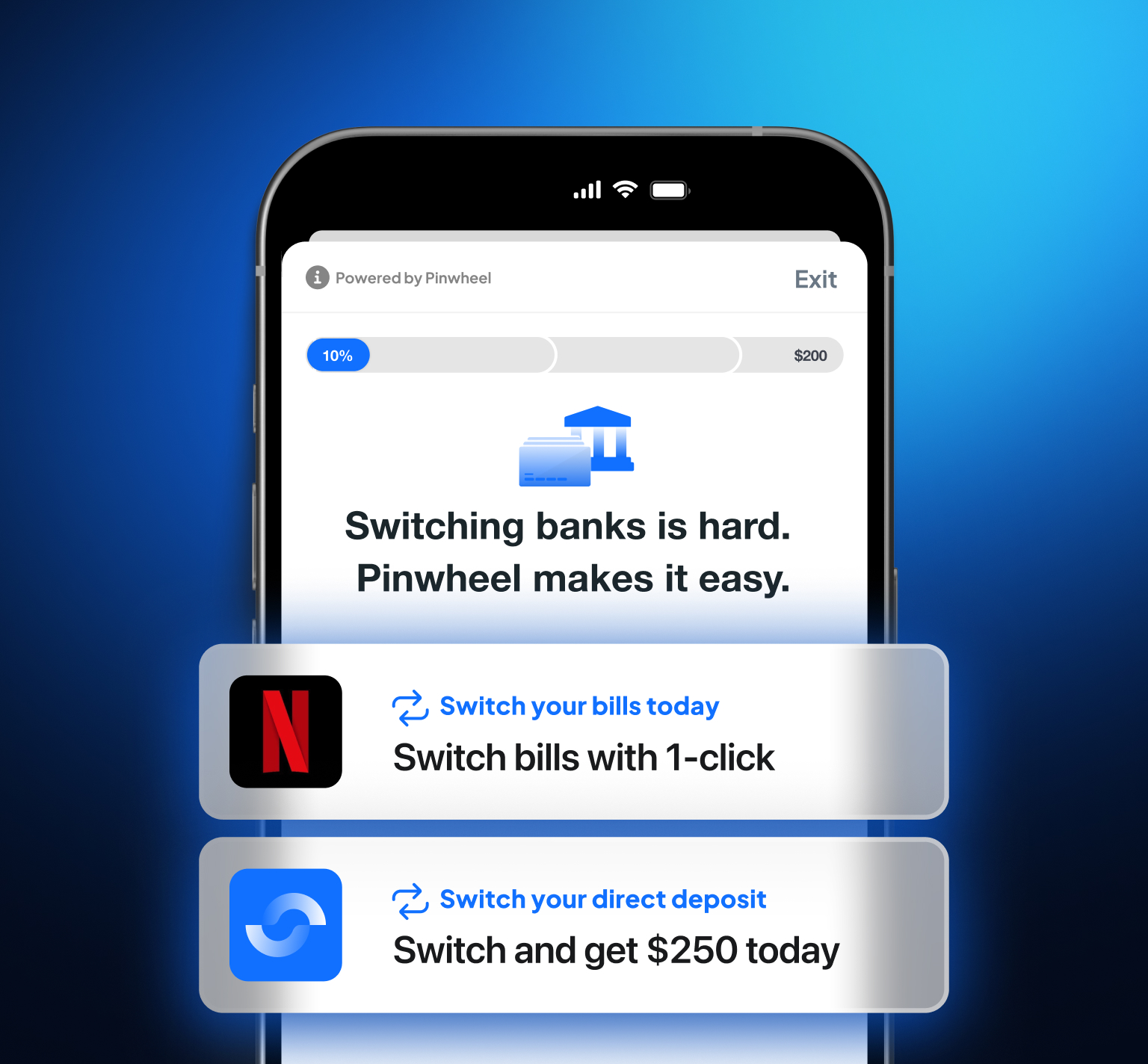

The Pinwheel Switch Kit is the industry’s only solution designed to establish true account primacy on day 1. This game-changing tool enables users to switch both their direct deposit and recurring payments to their newly opened account, helping them cut ties with their legacy bank. By integrating directly into the bank’s digital account opening flow, the Pinwheel Switch Kit captures new customers at the moment of intent.

Key features features of the Pinwheel Switch Kit include:

The highest converting deposit switch solution in-market:

Our conversion engine Pinwheel Prime delivers 30% more switches than any other provider and features the industry’s only 100% credential-less flow, made possible by our direct partnerships with prominent payroll providers.

Internal and external recurring payment detection:

Pinwheel’s proprietary algorithm automatically identifies bills with 80% more accuracy than competitors.

1-click payment switching:

Move both card and ACH-based payments to the new account with the most frictionless experience available.

Real-time transaction insights:

Enable timely notifications and reminders to progressively switch more bills with ongoing access to a customer’s linked account data.

Conclusion

With multi-banking behavior on the rise and digital convenience becoming table stakes, financial institutions must evolve their approach to primacy. To stay competitive, primacy can no longer be defined by direct deposits alone, and convenient digital solutions must be a top priority. The Pinwheel Switch Kit helps banks achieve true account primacy on day 1 through frictionless deposit and bill switching during account opening.

Curious to learn more about how the Pinwheel Switch Kit can help your institution improve account activation rates and drive primacy? Request a meeting.