.svg)

.svg)

In an era dominated by digital innovation, physical branches remain relevant—and even essential. While many national financial institutions are doubling down on digital channels and closing branches, 60% of new accounts are still being opened in person. This underscores a critical competitive differentiator for credit unions, who maintain a unique home town advantage. While the possibilities of digital self service are ever expanding, consumers are signaling that access to a branch in close proximity to their home is as important as ever. While pursuing necessary digital transformations, credit unions must protect their long-standing competitive advantage by continuing to invest in the branch experience.

Many Rushed To Digital

For decades, branches were the cornerstone of financial life in communities across America. However, by the end of 2023, the number of U.S. bank branches had declined by more than 20%, shrinking from around 100,000 to just 78,000 over the past 15 years. Meanwhile, online banks and financial technologies have captured significant market share, with the BAI Banking Outlook predicting that by 2026, 65% of all banking transactions will occur digitally.

While this may suggest local branches are becoming less common and less necessary, 60% of all accounts are STILL opened in the branch. Even with fewer branches. And the remaining branches are farther from consumers’ homes. While their top of the line smart phones offer account opening at home on their couch. Even amidst the digital revolution, there is an irreplaceable value of human interaction for certain types of transactions.

Few Have Bucked the Trend

Despite the move toward digital, some of the nation’s largest banks have surprised the industry by investing heavily in new branches. JPMorgan Chase plans to open 500 new branches in the next three years, while Bank of America is expanding into nine new markets across four states. Taking inspiration from community banks and credit unions that have historically differentiated with high touch, high familiarity human interactions, these two national banks have prioritized in person servicing “hubs.” By creating hubs where customers can solve more complex needs, they hope to complement consumers’ day-to-day digital first engagement. Banks investing in these hubs understand that even the most digital savvy consumers still want the comfort and security of being able to visit a branch. They hope these hubs will create a retention moat around customers who might otherwise switch to a neo bank with a slicker experience, but are wary of giving up access to a branch altogether.

Branches Remain In Demand

While older members may remain loyal to traditional banking experiences, Millennials and Gen-Z - who engage with financial institutions 3x more often than older generations - are digital first. However, even these younger generations continue to visit branches for high-touch, high-stakes interactions that can’t be accomplished as efficiently online.

Accenture’s 2023 Global Banking Consumer Study found that consumers visit branches to open accounts, seek financial advice, and access new products and services. Notably, 60% of respondents reported going to branches to resolve “specific and complicated problems.”

Even as digital channels have come to dominate day-to-day transactions, there is no denying that physical branches will continue to play an important role in some of the most important financial transactions of every consumer’s life. This is great news for credit unions, if they can maintain the personalized services and experiences consumers have long relied on them to deliver close to home.

Credit Unions Can Standout With Omni-Channel Capabilities

Today’s trends debunk recent expectations that consumers would shift to digital without looking back. Members from across generations have continued to demonstrate their preference toward in-branch engagement for interactions ranging from account opening, to issue resolution, to credit applications. While credit unions have long excelled at personalized service delivery in branch, they are still expected to modernize their digital capabilities to offer comprehensive account self-servicing capabilities. To succeed, they must deliver seamless, omni-channel experiences, where their expertise in human services seamlessly meets the emerging demand for digital convenience.

Each member interaction must now balance both worlds. If a member visits a branch to speak to a live representative, they will also expect the representative to access accurate, real-time account information and seamlessly execute tasks on behalf of, or in collaboration with the member - just as a member can do for his or herself online. Long waits, multiple representatives, multiple branch visits, or paper-based processing to complete a transaction are completely unacceptable.

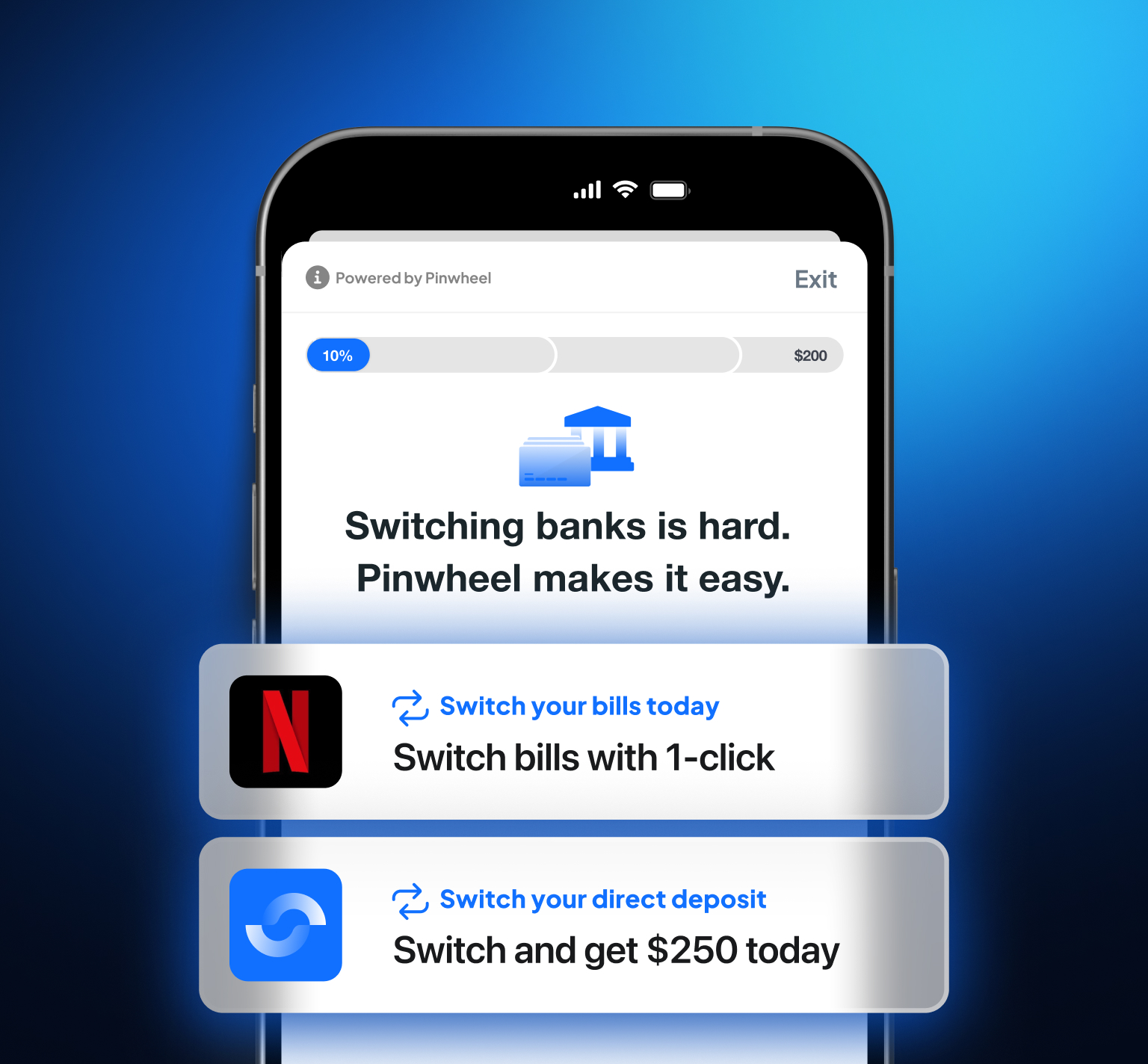

This is why we developed Pinwheel Smart Branch, which connects the convenience and security of a member’s device to streamline common in-branch transactions. A bank agent can offer a simple QR code to enable frictionless direct deposit enrollment at the time of account opening. Or instant verification for a credit application that would otherwise require burdensome document uploads. Pinwheel Smart Branch brings the power of digital banking to your physical locations.

Connect with us today to learn how Pinwheel’s suite of activation and engagement solutions can help you grow deposits, expand share of wallet, and win primacy.