.svg)

.svg)

In July 2022, the Wall Street Journal reported that global markets posted the “worst first half of a year in decades,” while economists say that the probability of a recession by June 2023 is 44%.

Although recent reports paint a gray picture of the future, not all companies struggle during economic downturns. For example, some of the most successful fintechs, such as Venmo and Block (formerly Square), were founded in the midst of the Great Recession.

So how can financial service providers today make sure their businesses continue to thrive in the face of challenging market conditions? According to Insider Intelligence, they should continue investing in tech and remain focused on improving the customer experience.

One way to put this into practice is through automated direct deposit switching, powered by payroll data connectivity APIs. It’s a solution that financial service providers integrate into their digital product, allowing their customers to seamlessly update their direct deposit settings in-app.

Although it may seem like a simple solution that helps consumers avoid manual processes, it has many benefits for financial service providers. The advantages of direct deposit switching go far beyond consumer convenience and can help banks and fintechs successfully navigate the current financial landscape.

Increase share of wallet and profitability

An automated direct deposit switching solution powered by a payroll API makes it easy for you to grow deposits. This is essential to increasing customer lifetime value (and, by extension, profits) because it holds the key to becoming a customer’s primary financial institution (PFI). In fact, 43% of consumers say their PFI is the institution where their paycheck or social security is deposited, and 93% of US workers are paid via direct deposit. This opens doors to customers investing in additional services like loans, insurance, or financial management tools.

When customers fund their accounts, engagement rises, which also helps financial service providers grow profits. More deposits equal more debit card usage, which positively impacts interchange revenue. If you have 2,000 customers switch $500 of each paycheck into your institution, that's an increase of $26M deposits in only one year. It’s not surprising that one of the most successful names in fintech, Cash App, drove its growth in early 2022 with direct deposits alongside the growing use of its debit card.

Above and beyond this, financial service providers may find that investing energy to get existing customers to switch their direct deposits can convert a potentially negative LTV customer into a positive one. This is critical, particularly in the neobank segment, where many players in this space have been optimizing towards customer acquisition at the expense of profitability. Implementing automated direct deposit switching can potentially help these players finally achieve profitable growth.

Lower customer attrition

APIs that automate direct deposit switching also enable direct deposit allocation monitoring. The monitoring feature allows financial service providers to see who else holds a share of the customer’s direct deposit. With this kind of data, they can proactively answer their customers’ needs before they completely switch to another provider.

Thanks to technology, consumers today can quickly open new bank accounts. While convenient, this has created “hidden attrition.” Customers open new accounts with different financial service providers, and their PFI doesn’t notice until it’s too late. Hidden attrition leads to revenue loss, as research by Bain & Company has found that banks lose out on customers for high-margin products like loans and investments.

Real-time customer direct deposit data isn’t just essential for retention — it can also help banks and fintechs prepare for financial turbulence. “One of the characteristics [of organizations most prepared for a recession] is clarity of strategy and focus and an understanding who the customer or member base really is,” explains Ron Shevlin, Chief Research Officer at Cornerstone Advisors. For example, a financial provider who notices a large segment of their consumer base is allocating their deposits with a competitor could accelerate the development of marketing campaigns and features to try to retain those consumers.

Ensure loan repayments

In the current market conditions, many lenders will switch their focus from growing their consumer base to lowering default risk and improving collections. Lenders with consumer-permissioned access to the borrower’s direct deposit can make sure the loan is repaid on time, minimizing the risk of missed payments.

Loans that are linked to the borrower’s paycheck (also known as paycheck linked lending) use payroll data connectivity APIs to automate the repayment process via the direct deposit. Once the consumer connects to their payroll or income platform, the loan will automatically be deducted from their paycheck, which has a beneficial impact on repayments.

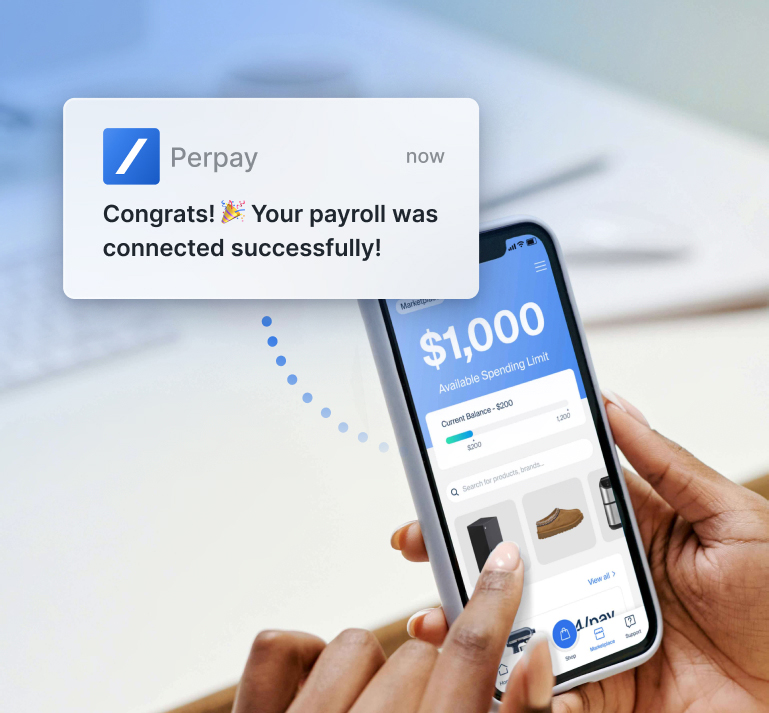

Perpay, a “buy now, pay later” marketplace, was able to increase repayment rates by 3x once it set up paycheck linked lending. The solution also lowered acquisition costs and increased conversion speed for the company, which are major advantages in an economic crisis.

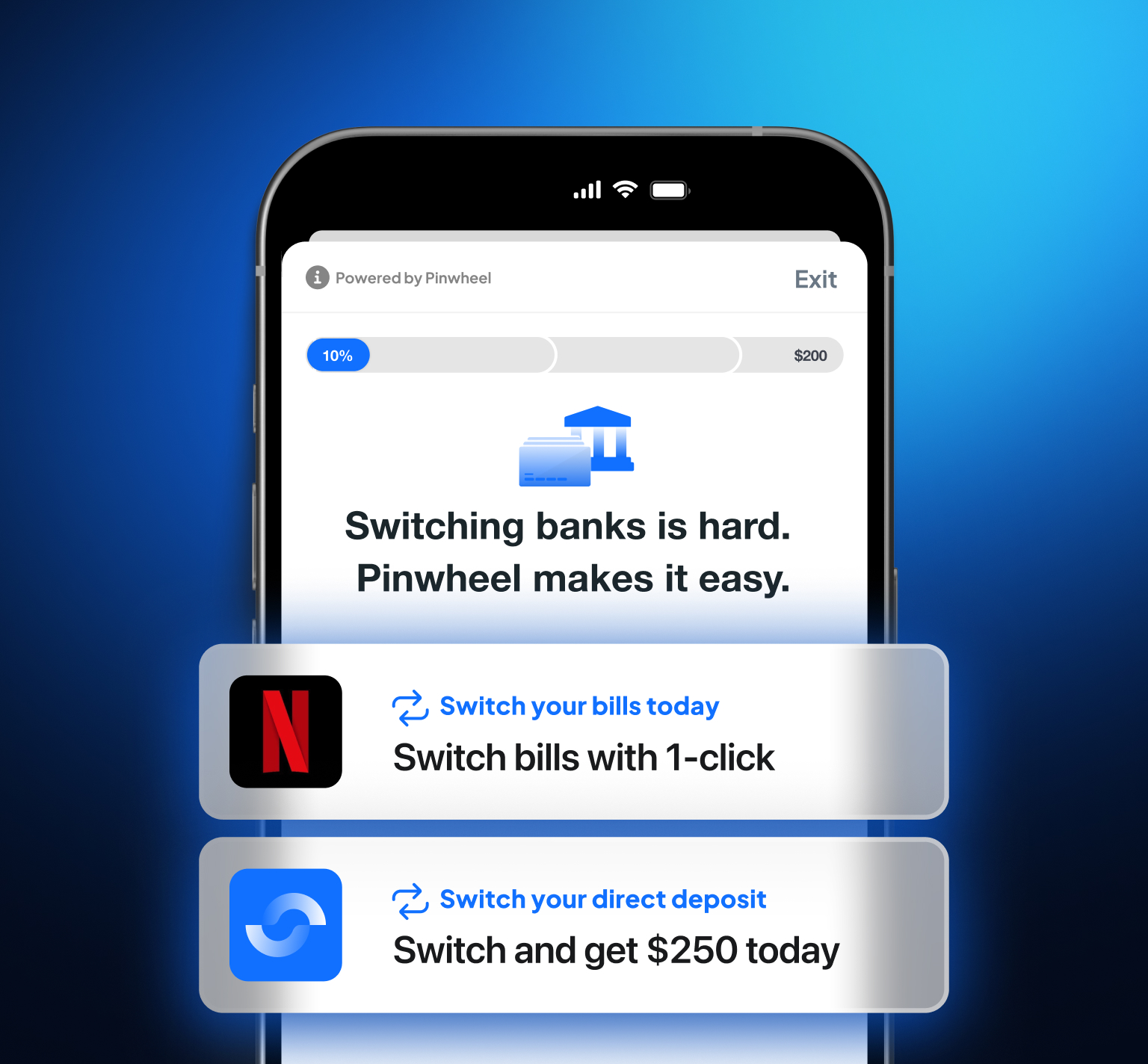

How Pinwheel automates direct deposit switching

Economic downturns test financial providers’ resilience and ability to adapt to a changing market and consumers’ needs. Tech solutions make this easier by providing tools that allow them to better understand their customers and speed up innovation and the development of new products.

Financial service providers who want to offer a frictionless direct deposit switching process can rely on APIs such as Pinwheel’s to do the heavy lifting. We connect to over 1,600 income and payroll platforms and also provide connectivity to 1.5 million employers, more than any other API provider in the industry, preventing customer frustration over insufficient coverage and materially improving conversion for our clients.

Our clients can build a custom user experience that fits seamlessly into their digital banking service, whether it’s a lending product or a slick mobile banking app. Then the customer can connect to their payroll or income platform in a couple of clicks and direct a portion or the entirety of their paycheck to their bank account.

Once the direct deposit is set up, the financial provider can leverage this single point of connectivity to monitor deposit allocations and gain important insights into the kind of services their customers need, helping earn their trust and loyalty.

As experts in this space, we partner with our clients throughout the process. For example, we advise them on best practices with a comprehensive direct deposit switching marketing toolkit to help win share of wallet and grow profitability.

To learn more about how Pinwheel’s API can help you navigate the current market conditions, download our ultimate guide to direct deposit switching or contact us here.